With cryptocurrency prices increasing, many investors are looking to take profits off the table. This article covers what you can do to minimise the amount of tax you will pay. In short, be strategic about when and the amounts you cash out, but it requires careful planning and an understanding of how the profit is calculated. A key conclusion is that while tax planning is essential, it shouldn’t override fundamental investment decisions if there’s a strong potential for additional gains.

Let’s look at an example.

Example 1

Jill’s crypto portfolio is currently worth $400,000, but her initial investment (cost basis) was $200,000. This means she has a $200,000 unrealised profit. For simplicity in this example, we’ll assume that Jill has no other income and only one token with an unrealised gain.

Tax Implications in New Zealand

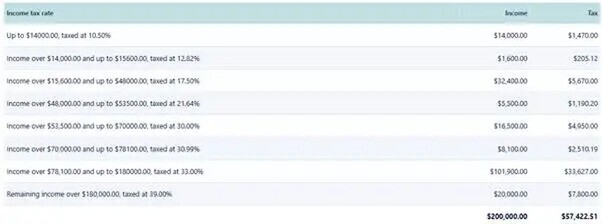

New Zealand’s progressive tax system means higher income is taxed at higher rates. If Jill cashes out all her crypto today (February 2025), that entire $200,000 profit will be taxed in the 2025 financial year. This could push some of her income into the higher 33% and 39% tax brackets.

The total tax that Jill would pay is $57,422.51

A Tax-Efficient Strategy

Instead, Jill could split her crypto sales: half in the 2025 tax year (today) and half in the 2026 tax year (after April 2025).

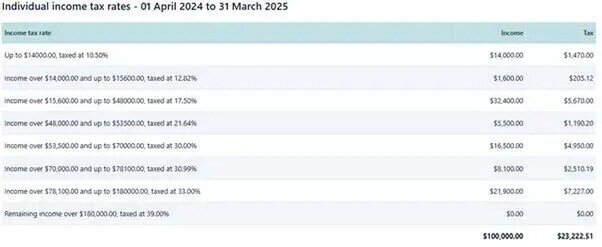

Under this option, the total amount of tax Jill would pay is $46,445 (i.e., $23,222 multiplied by two years)

This is a tax difference of ~$11k for $200k of profit (of 5.5% savings).

This strategy may offer several advantages:

Reduced Tax: By spreading the sales, Jill can significantly reduce her overall tax liability. In this example, splitting the sale could save her over $10,000 in taxes.

Lower Tax Brackets: Splitting the sales helps Jill avoid the highest tax bracket (39%) and limits the amount taxed at 33% or a lower marginal tax rate. It utilises her lower marginal tax rates at 10.5% and 17.5% over two financial years. This is the reason why she can save taxes.

Time Value of Money: Deferring half the tax payment to the 2026 year gives Jill more time to be productive with those tax funds. She could earn interest from the bank on her tax money. The tax payment for the 2026 financial year would be due on 7 May 2026 (on the basis that the 2025 tax return is filed after 15 January 2025).

Provisional Tax Considerations

If someone’s residual income tax exceeds $60,000, they automatically become a provisional taxpayer. If Jill sells all her crypto at once and her tax bill is over $60,000, the IRD (Inland Revenue Department) expects her to pay the tax in instalments throughout the year. Failing to do so can result in interest charges and penalties, further increasing the total tax owed. Splitting the sale can help prevent this situation.

Market Uncertainty

Of course, this example assumes that Jill’s portfolio remains consistent both now, and in April 2025. Cryptocurrency has rapid price fluctuations, and we know that the portfolio could be any value (your crystal ball is likely better than ours!). Let’s take a look at a couple of further examples to emphasise that tax strategy is only a small part of the equalisation to consider; market prices have a much larger effect.

Example 2

Jill’s crypto portfolio is currently worth $400,000 in February 2025, but her initial investment (cost basis) was $200,000. This means she has a $200,000 unrealised profit.

In this example, she decides to cash out $200k now (February 2025) to try to split her profit over two financial years and prevent having to pay tax at the 39% tax rate.

In April 2025, her remaining cryptocurrency (which was $200k in February 2025) is now worth $300k, and she has cashed out.

In the 2025 financial year, Jill has a taxable profit of $100k. Profit = sale value ($200k – being 50% of the portfolio) less purchase value ($100k – being 50% of the portfolio).

Her tax to pay is $23,222

In the 2026 financial year, Jill has a taxable profit of $200k. Profit = sale value ($300k – being 50% of the portfolio) less purchase value ($100k – being 50% of the portfolio).

Her tax to pay is $57,422

In summary, her total profit is $300k, and total tax bill is $57,422.

The tax is 19.14% of her profit, and the after-tax profit is $242,578.

Example 3

Rather than trying to spread profit during both financial years. Jill thinks that cryptocurrency prices will continue to increase between now and April 2025. She is aware that if she cashes out all at one time, you will pay tax at a higher rate.

Jill decides to forgo the immediate sale in February and instead cashes out her entire portfolio in April 2025 for $600k. This is the same price as example 2, but now she cashes out 100% of the portfolio rather than 50%.

Profit $400k = sale value ($600k) less purchase value ($200k)

Tax on $400k in a single financial year is $135,423

In summary, her total profit is $400k and her total tax bill is $135,423.

The tax is 33.86% of her profit, and the after-tax profit is $264,577.

Summary

The higher actual profit from price appreciation ($400k vs $300k) more than compensated for the higher tax rate in Example 3. This demonstrates that tax efficiency, while important, shouldn’t necessarily be the primary driver of investment decisions. In this case, staying invested for the full price appreciation was more valuable than optimising the tax rate.

The strategy of splitting sales provided some risk management benefits by locking in partial profits earlier, though this came at the cost of potentially missing out on further gains (which didn’t happen in this case but could have).

The main conclusion is that while tax planning is important, it shouldn’t override fundamental investment decisions if there’s a strong potential for additional gains. In this scenario, the benefit of capturing the full market upside outweighed the tax advantages of splitting the sales across tax years.

Are you ACTUALLY crypto tax compliant?

70% of crypto holders are not tax compliant.

They're risking massive tax penalties — potentially losing hundreds of thousands in fines, fees, and audit nightmares.

12 questions | 2 mins | PDF report directly to your inbox.

Find out now

Contact Us

Contact Tim Doyle for a call or meeting to discuss any cryptocurrency tax or accounting questions. Our office is in Cambridge, Waikato, or we can arrange a video conference call.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.